On July 17, 2020, the Government of Canada released draft legislative proposals to extend and significantly change the Canada Emergency Wage Subsidy (CEWS). The main changes proposed for the CEWS are summarized below. For a more comprehensive overview of the changes, please see our July 2020 Blakes Article: Government Proposes to Extend and Overhaul the Canada Emergency Wage Subsidy.

Extension of the Program

The proposals would extend the CEWS for an additional 12 weeks, to November 21, 2020. The government simultaneously announced an intention to extend the CEWS until at least December 19, 2020, though this was not included in the draft legislation.

Changes to Calculation of the Subsidy

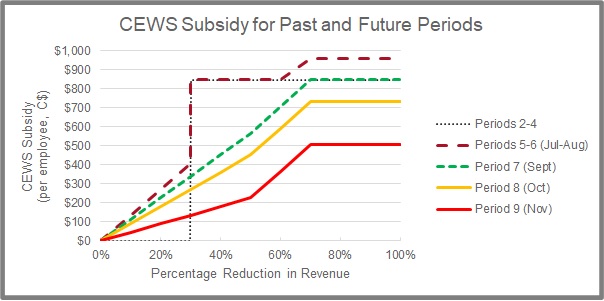

The proposals would change the qualification criteria and amount of subsidy provided. Previously, only eligible employers that met a revenue reduction threshold—generally, at least a 30 per cent reduction from baseline—were entitled to a subsidy, but the subsidy did not otherwise vary based on revenue loss.

The proposed changes would allow any eligible employer experiencing a revenue decline to obtain a subsidy, but the amount of subsidy will be based on the degree of revenue loss and will gradually decline each month, starting in September 2020. An additional subsidy will apply to employers that have suffered a severe—being greater than 50 per cent—revenue loss over a sustained period. For the July and August periods, employers can continue to rely on the old rules if they would have resulted in a larger subsidy.

To illustrate, the following chart shows the potential subsidies that would be available to an employer that has suffered a constant revenue loss since the second CEWS period.

Technical Changes

The proposals also include a number of technical changes and corrections to the CEWS, including changes to the range of eligible employers and employees and the calculation of revenues, fixes to allow for amalgamations and acquisitions, and new anti-abuse rules.

For further information, please contact a member of our Tax group.