Welcome to the March edition of Blakes upRound, a regular publication from the Blakes Emerging Companies & Venture Capital (EC&VC) group that highlights legal developments relevant to venture investors and emerging companies and provides concise insights on recent trends and market developments.

The Blakes EC&VC group is a nationwide practice with lawyers in Toronto, Calgary, Vancouver and Montréal providing transactional and ongoing legal assistance to some of the most dynamic emerging companies in Canada and venture investors from Canada, the United States and beyond. As a full-service business law firm, Blakes provides advice on all aspects of Canadian law relevant to our clients. Our EC&VC practice includes Blakes Ventures, an innovative service offering to support the entire emerging company ecosystem, and Nitro, our legal support program for early-stage companies and founders.

In this Edition

How to leverage your intellectual property and protect the value of your innovations

Potential online content regulations, comprehensive guidelines for compliance with fintech and payments regulations, and other need-to-know topics

Paul Ciriello on the market for venture capital in 2024

Health-care and biotech bright spot in 2023 deal data; hope for markets to turn later this year

Market Insights

Intellectual Property 101 — For many startups and scaleups, intellectual property (IP) is crucial to the company’s competitive advantage and, therefore, its overall success and value. This bulletin provides a refresher on the common categories of IP in Canada and best practices for protecting and leveraging IP that companies should implement and investors should seek.

Founders and investors may find the following insights from our Blakes colleagues helpful and instructive:

Online Harms Act — On February 26, 2024, the federal government tabled Bill C-63, which would enact the Online Harms Act (Act) and establish Canada’s first federal online content moderation regime. The purposes of the Act include mitigating the risks posed by harmful content online, protecting children’s physical and mental health, holding online platforms accountable and rendering certain egregious forms of harmful content inaccessible. To learn more about this new Act, read our Blakes Bulletin: Canada’s Bill C-63: Online Harms Act Targets Harmful Content on Social Media.

Cybersecurity — It has been said many times before, but it cannot be said enough: the most effective way to avoid cybersecurity threats is to remain vigilant and prepared. Cyberattacks are constantly evolving, and organizations must adapt to mitigate the risk of a breach and the damages that come with it. Read our Blakes Five Under 5: Preaching to Evade Breaching: The Latest Trends in Canadian Cybersecurityto learn about the most significant developments in cybersecurity regulations, case law and best practices for managing cyber threats.

FinTech and Payments Guidelines — On February 21, 2024, the Bank of Canada released draft supervisory guidelines on the Retail Payments Activities Act, reflecting the Bank of Canada’s expectations of payment service providers (PSPs). Compliance with the guidelines would be onerous and require PSPs to have extensive financial resources. Due to that financial burden, startups will likely be impacted the most, potentially hindering their entry into the Canadian payments space and leading to less competition and innovation. PSPs have until May 21, 2024, to submit their comments. Read more about these guidelines in ourBlakes Bulletin: Highlights From Bank of Canada’s Draft Guidance on Retail Payment Activities Act.

Fund Formation and Investment Trends — In 2023, private capital pooled funds continued to be an excellent vehicle for investment in different asset classes while allowing for diversity of investments. Last year, fund sponsors continued to raise large amounts of cash to deploy. Read our Blakes Bulletin: Five Trends in Private Capital Fund Formation and Investmentto learn about some of the most significant developments in private capital funds in 2023.

How do you see the market for venture capital so far in 2024?

While the overall venture market continues its cautious pattern so far in 2024, investing in seed stage, anything.ai, cybersecurity and data-driven businesses remains strong in Q1.

We continue to live through the transition from the last major tech and investment cycle to the next one. It seems clear that we are already in the early phases of the next cycle — one that is characterized by the race to develop core AI and machine learning technologies, the application of these technologies in every industry and functional area of work and life, and the evolution of new capabilities among next-wave cleantech and platform-based life sciences companies.

The pace of investing is likely to accelerate later in the year as interest rates decline, corporate development activity revives, private equity dealmaking and secondary transactions provide liquidity, and confidence grows in the new market cycle. New companies will spring up — in the e-commerce cycle, for example — that challenge incumbents. At the same time, incumbents will move to adapt their businesses to the new world.

New funds are being raised by venture capitalists, especially by firms raising their third fund or higher. For first-time funds, it is taking longer to raise their sophomore funds as limited partners carefully evaluate their portfolios, and more than the historical average number of first-time funds may not make it. Secondary funds have continued to attract record capital levels as the target market has expanded in the past 18 months.

Overall, I expect that companies responsive to the new market cycle dynamics will have an easier time finding capital and will get the jump on building value — good news for those founders and investors.

If you would like to hear from Paul Ciriello, Strategic Advisor to Blakes and our clients, please submit your questions here.

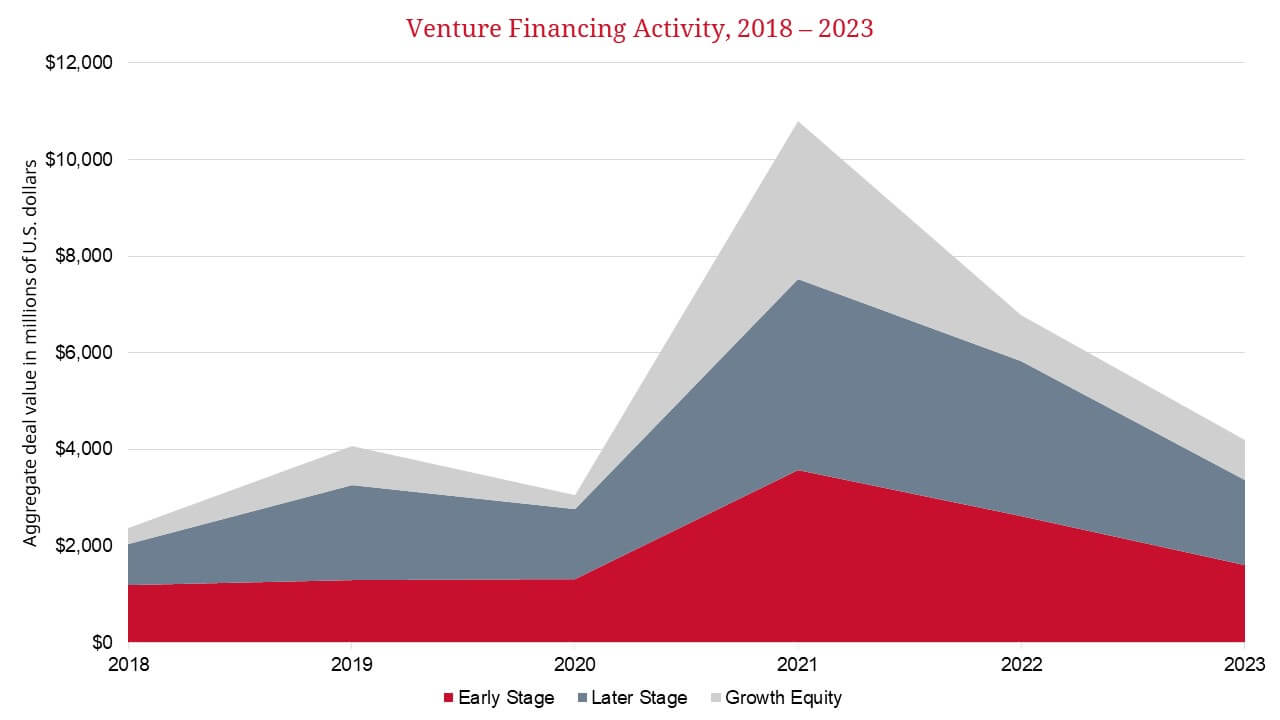

Deal Monitor

Data sourced from PitchBook.

With the full data for 2023 now in, we can see that health care and biotechnology was another bright spot in the Canadian venture and growth equity market. Among the largest transactions was Vancouver-based Aspect Biosystems’ strategic partnership with Novo Nordisk to develop bioprinted tissue therapeutics for diabetes and obesity. The deal included US$75-million in upfront payments and will include up to US$650-million in future milestone payments per product arising from the collaboration.

Other large biotech transactions in 2023 included Abdera Therapeutics’ US$110-million Series B led by venBio Partners, DalCor Pharmaceuticals’ US$80-million Series D from Investissement Québec and others, BenchSci’s C$95-million Series D led by Generation Investment Management and Synaptive’s US$50-million financing round led by Export Development Canada.

The end of 2023 and the beginning of 2024 have remained relatively slow. We continue to see companies being creative, doing more with less, delaying financing, accepting flat rounds and taking additional investment from existing investors.

With the U.S. Federal Reserve, Bank of Canada and other central banks expected to cut interest rates later this year, there is hope for an approaching increase in investment activity and a turn in the venture and growth equity market.

Blakes and Blakes Business Class communications are intended for informational purposes only and do not constitute legal advice or an opinion on any issue. We would be pleased to provide additional details or advice about specific situations if desired.